Ambulance bills are one of the most common surprise medical bills in the US healthcare system. You didn’t choose the ambulance. You couldn’t. You were having an emergency.

And yet here you are, holding a bill for hundreds or thousands of dollars from a company you’ve never heard of.

This guide explains why that happens, what the law actually covers, and what your options are - including why the type of insurance you have matters.

When you call 911, you have no say in which ambulance company shows up. The dispatcher sends whoever is available. That company may or may not be in your insurance network — and you have no way to check in the middle of an emergency.

This is the root of the problem. Ambulance providers — especially private ones — often operate outside insurance networks. When they do, they can bill at their full rate. Your insurance pays what they decide is “reasonable.” You get stuck with the rest. That gap is called balance billing. Here's an example of how it works:

Whether you can fight it - and how - depends heavily on what type of ambulance you took and what type of insurance you have.

The federal No Surprises Act does not fully cover ground ambulance services. Air ambulance is a different story.

If you took an air ambulance and yours was processed as out-of-network, you likely have strong grounds to dispute it. But if you took a ground ambulance, it might be tougher. Congress left ground ambulance out of the No Surprises Act. The Advisory Committee on Ground Ambulance and Patient Billing (GAPB) released recommendations on how best to protect consumers from surprise billing for emergency ground ambulance services, but right now, there are no federal laws capping what ground ambulance companies can charge you. However, many states have implemented state protections based on these recommendations, but whether they apply to you depends on the type of insurance you have.

There are two main types of commercial health insurance in the US. They look the same from the outside but operate under completely different legal frameworks.

Not sure which type you have? Check out our guide to Insurance Types to explain the difference and how to find out.

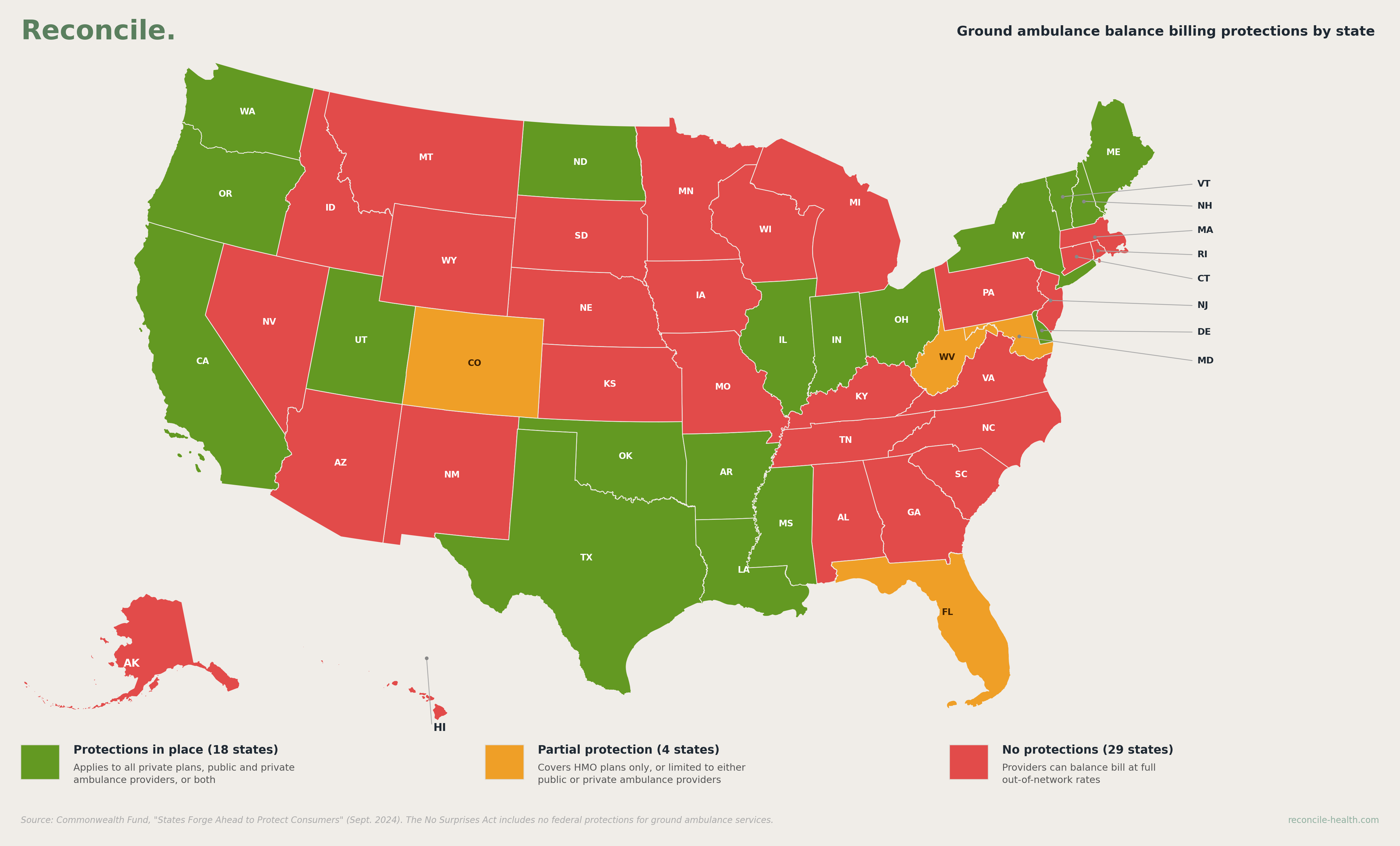

State balance billing laws apply to you. About 20 states have meaningful ground ambulance protections, with 4 more offering partial coverage.The map below shows where those protections exist.

Click to expand

If your state has protections and you were balance-billed, you have a legal basis to dispute the charge.

Here’s the hard truth: if your insurance comes from a large employer — most companies with more than 200 employees self-insure — your state’s ground ambulance laws almost certainly don’t apply to your plan. ERISA,the federal law that governs these plans, generally blocks states from regulating them.

That means even if you live in California or New York — states with strong ambulance protections — those protections may not cover you.

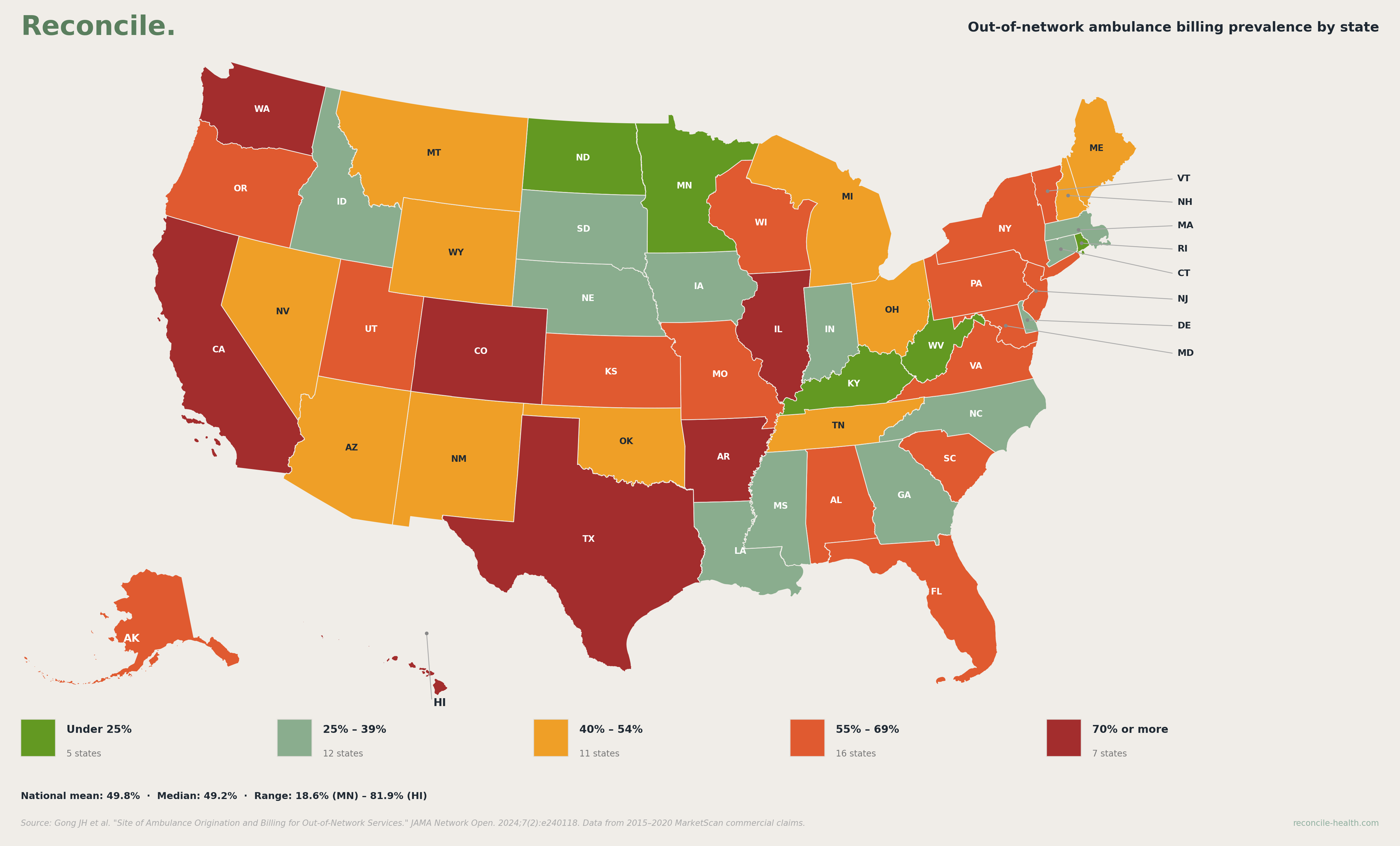

The second map shows the real-world picture for self-insured plan members. It shows the actual prevalence of out-of-network ambulance billing.

Click to expand

The national average is close to 50%. In states like Colorado, Illinois, Texas, Washington, and California, more than 70% of ground ambulance rides result in an out-of-network bill. Even in “protected” states, the real-world out-of-network rate is high — because those state protections don’t reach self-insured plans.

Regardless of your type of insurance, always request the following two things as the starting point:

From these two documents, Reconcile can conduct a proper review of the bill. Here are our steps:

Reconcile leverages its expertise in medical coding & billing to flag potential errors. Some common ambulance billing errors include:

Your Explanation of Benefits (EOB) shows what your insurer paid and what they say you owe — but it doesn’t tell you whether the claim was processed correctly. Reconcile will check:

If the bill is valid but higher than it should be, negotiation is the next step. Ambulance billing companies have internal programs for financial hardship, reduced settlements, and payment plans — none of which they advertise.

This is exactly what Reconcile was built to handle. We review your bill line by line, check your EOB against your plan terms, flag every error and overcharge, and then take the dispute forward on your behalf — so you don’t have to spend your evenings on hold with a billing department.